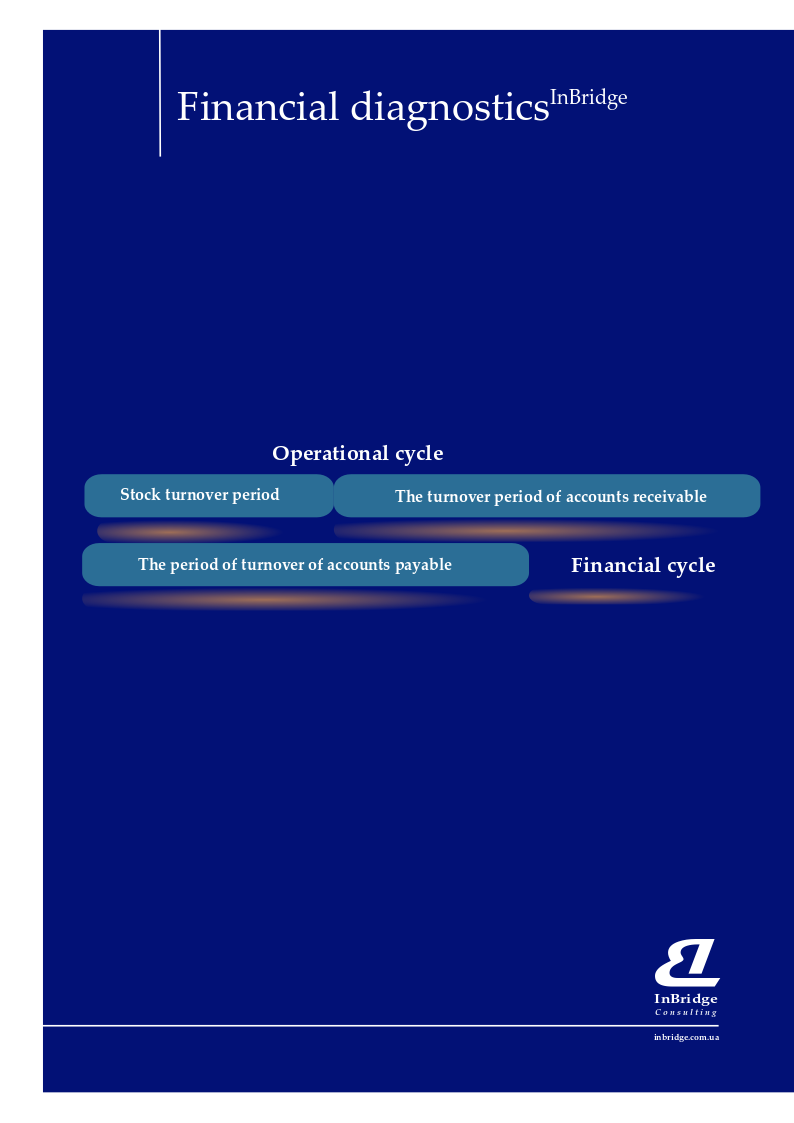

The duration of the operating cycle is one of the important indicators that characterizes the Company's business activity. The value of this indicator indicates the duration of the period during which the Company acquires raw materials, manufactures finished products, stores them in stock until the moment of sale and receipt of funds for the goods shipped. The less the duration of the operating cycle, the more effective the company's activities, the higher its business activity. The duration of the operating cycle is calculated by adding the period of turnover of stocks and receivables.

The duration of the operating cycle is one of the important indicators that characterizes the Company's business activity. The value of this indicator indicates the duration of the period during which the Company acquires raw materials, manufactures finished products, stores them in stock until the moment of sale and receipt of funds for the goods shipped. The less the duration of the operating cycle, the more effective the company's activities, the higher its business activity. The duration of the operating cycle is calculated by adding the period of turnover of stocks and receivables.

The financial cycle is a period that begins at the time when suppliers pay for raw materials and materials (repayment of accounts payable) and ends at the time of receipt of funds for the goods shipped (payable payable). The average value of the duration of the financial cycle is calculated as the sum of the period of turnover (repayment) of accounts receivable and inventories with the deduction of the period of turnover (payment) of accounts payable. The higher the value of the financial cycle, the higher the company needs in cash to purchase working capital. The optimum value of this indicator is equal to zero or a negative value, which indicates that the Company has cash to finance its current operations. Lack of the required amount of funds leads to the need to attract borrowed money in the form of bank loans, which leads to the emergence of additional costs in the form of interest payments. It is possible to warn this situation by identifying the main factors that affect the cash flow shortage.

The main factors affecting the duration of the financial cycle are a decrease in the period of turnover of stocks, accounts receivable and increase - payable. Generic indicators that indicate unwanted financial cycle length may be low profitability or negative trend and negative cash flow. The following factors influence the low profitability or negative trend of it:

- volumes of sales undesirable influence, "treated" by optimization of assortment, marketing measures;

- price of a product - marketing measures, pricing;

- production and non-production costs - cost management.

In turn, the negative cash flow is influenced by the growth of stocks, receivables, decrease in payables, undesirable effects of which are eliminated by the establishment of a control system for cash and other working capital.

Consequently, optimization of the product range and price policy of the Company, introduction of a management system of expenses and circulating assets will allow to reduce the duration of the financial cycle to the normative value and eliminate the lack of funds.

By nBridge Consulting, the financial cycle, the factors that determine its duration and shape the trend, are investigated during the extended financial diagnostics of the company.

In addition, based on the results of the financial diagnostics of the company, draft management decisions are provided to classify the duration of the financial cycle of the Company in the zone of optimal values.

Application. The procedure for providing financial diagnostics services to the company.